The 2008 Financial Crisis: The collapse of Bear Stearns

and the rescue of AIG

and the rescue of AIG

Introduction

One of the greatest economic disaster that happened after the great depression, 1929, was the 2008 financial crisis. This phenomenon led to a great regression in the US and affected many lives. To illustrate, the housing price in the US plummeted 31.8 percent, and the unemployment rate rocketed. Even though two years after the recession ended, the unemployment rate was still above 9 percent. (1) In this blog, we will try to explore the cause of this 2008 financial crisis, and why a gigantic investment bank, Bear Stearns, collapsed. Finally, we will look at an action of the Federal Reserve that poured almost 200 $ billions in order to bail out a well-known insurance company (2), American International Group (AIG), from the verge of bankruptcy.

Brief summary of the crisis

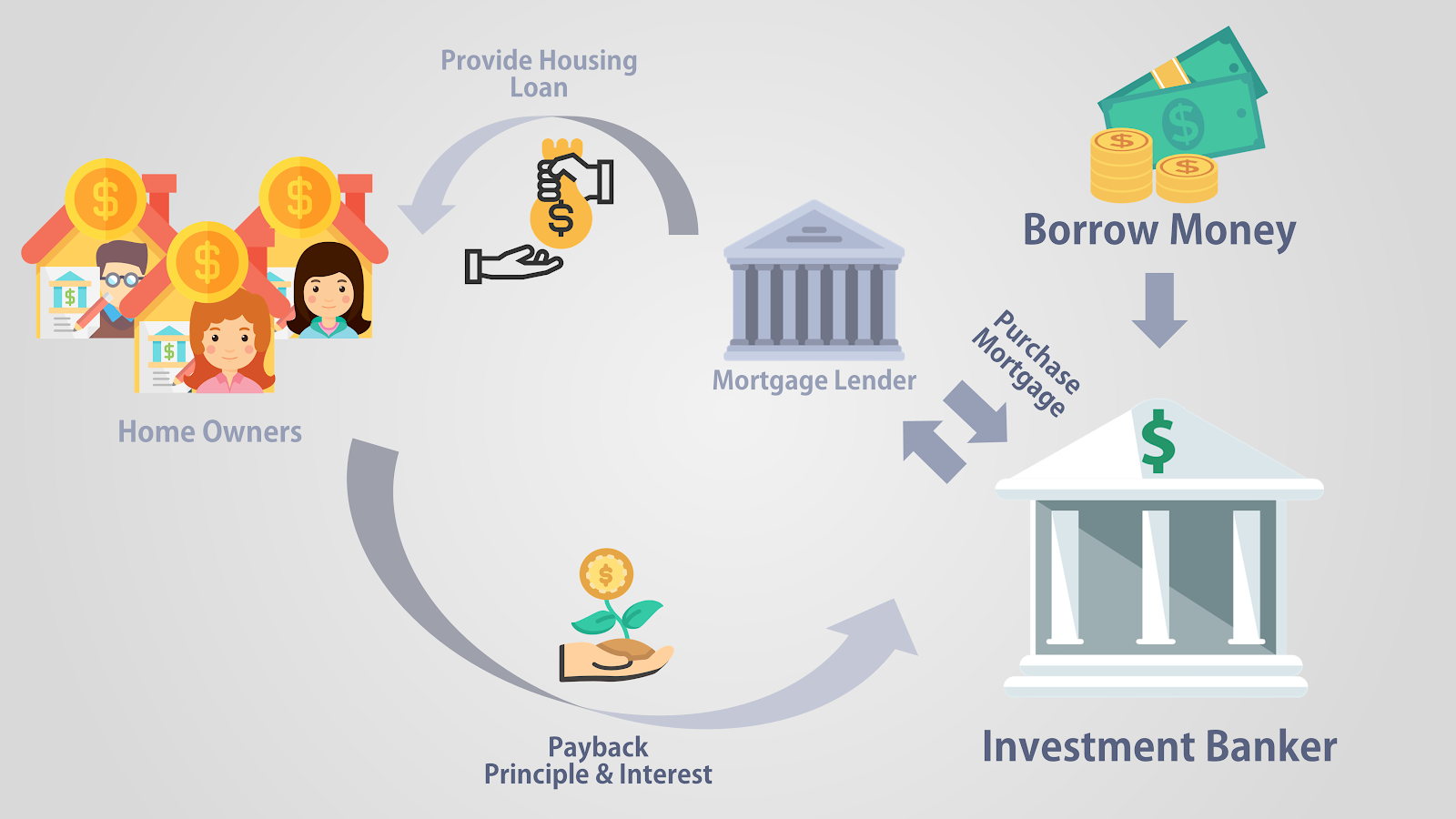

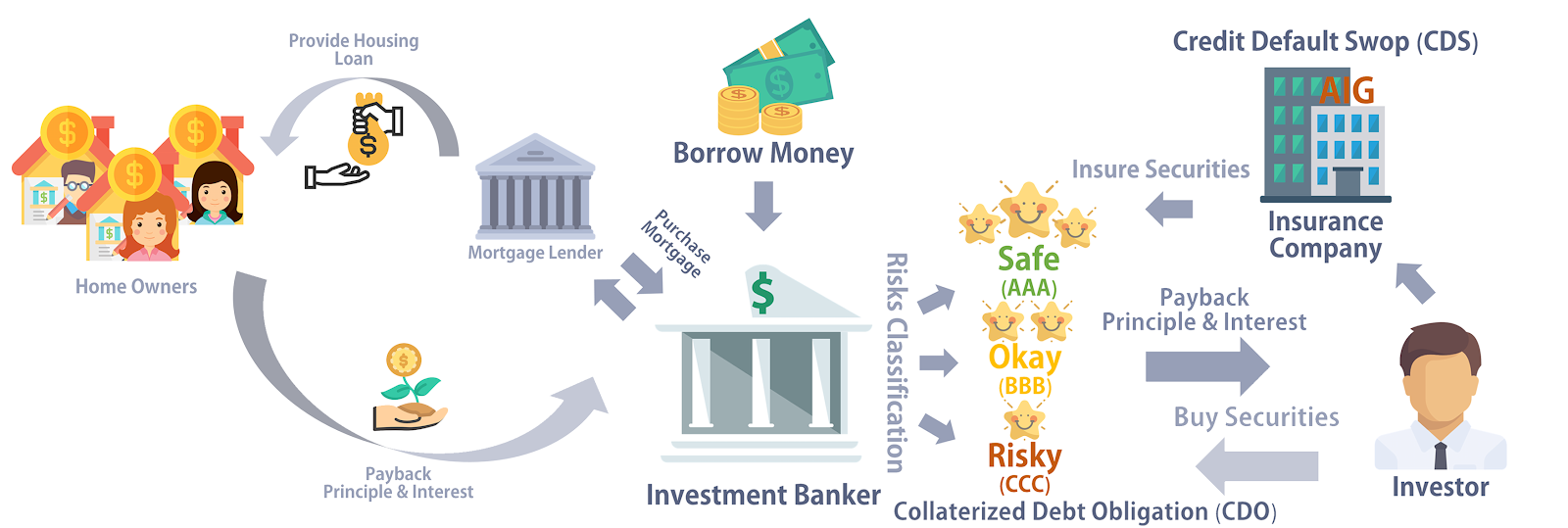

Imagine you want to buy a house, most of the people rarely buy a house with cash. They usually contact a bank to ask for a mortgage, a housing loan. The bank will make sure that the borrower has a potential to pay back the loan by checking his/her financial status, and if he/she passes the qualification, the transaction for a mortgage will be made.

The chaos starts to occur when the third party gets involved. At that time, the interest rate was very low, only about one percent, and there was a huge amount of money surplus from other countries. These make the cost of borrowing money become very cheap (3). Investment banks saw an opportunity for this event, so they join this cycle by borrowing money to purchase thousands of mortgages from the bank. This means that Investment bank will receive thousands of payment from the home owners.

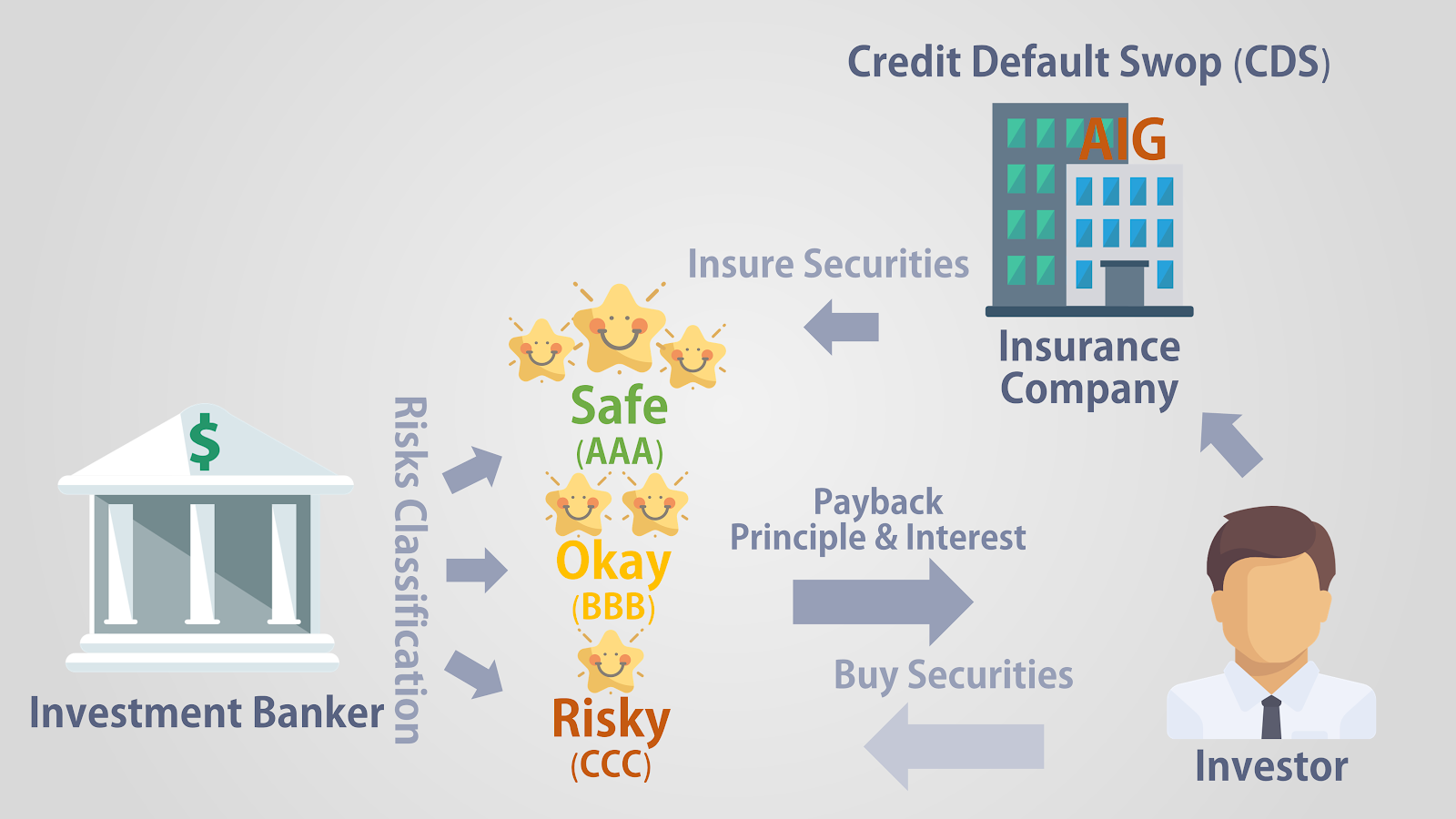

After buying mortgages from the bank, the investment bank those mortgages into Collateralized Debt Obligation (CDO). In other words, they categorize those mortgages by risk and sell them to the investor. Like we have learned in class, a riskier security should have a higher expected return. Therefore, the rating agencies are hired to assess the riskiness of the CDO. The riskiness of security was transferred into a letter grade, for example, AAA, BBB, and CCC. With AAA is the safest and BBB, and CCC are less safe respectively.

To make the security even safer, the new financial product so-called Credit Default Swap (CDS) was introduced to the investor by insurance companies. This product works like an insurance. To clarify, if the CDO defaults, investors who have bought CDS still receive money from an insurance company.

|

| The whole process will look like this following |

Investors really like CDO security; they want more, but the problem is that there are limited people to buy a house. Therefore, the mortgage lender did things that they should not do. They lessen the qualification of people who want to buy a house or let people buy a house without any down payment in order to attract people to buy more house.This practice works for short term, but in the end, people buy houses for speculating not for living. As a result, when the housing bubble burst, many homeowners abandoned their house; the houses’ price plummeted, which affect many financial institutions and investors who have CDO in their portfolio. Also, the collapse of CDO cause insurance companies that issued Credit Default Swaps like AIG get into troubles. Finally, the negative impact of this housing sector spread widely and lead to the 2008 financial crisis.

What's the timeline of important events from the beginning of 2008 to the end of the crisis?

These following are some of the interesting events that happened during this crisis;

In 2007, Housing crisis deepens. Banks and funds that invested big in subprime mortgages are left with worthless assets as housing price fell.

July 31, 2007: Investment bank Bear Stearns close two hedge funds that invested in risky securities backed by subprime mortgage loans.

January, 2008: Existing home sales rate fell to its lowest level in 10 years.

March 16, 2008: The Federal Reserve agrees to guarantee $30 billion of Bear Stearns'

assets, so that JP Morgan would purchase it and prevent the company from bankruptcy

September 15, 2008: Lehman Brothers Bankruptcy Triggered Global Panic

September 16, 2008: The world's largest insurer, American International Group accepts an $85 billion federal bailout that gives the government 79.9% stake with the company.

September 25, 2008: Federal regulators close Washington Mutual Bank and its branches and sold assets to JPMorgan Chase in the biggest U.S. bank failure in history.

October 7, 2008: The Federal Reserve decided to directly issue short-term loans for businesses that can't get them elsewhere with the total about of $1.7 trillion.

October 21, 2008: The Federal Reserve lends $540 billion to bail out money market funds

The collapse of Bear Stearns

The impact of this financial disaster was so dramatic. Even a well-known investment bank was wiped out as a result of this event. The Bear Stearns Companies, Inc. was a New York-based global investment bank. In 2006, it produced $9 billion in revenue, earned $2 billion in profits, and employed over 13,000 employees worldwide. However, its demise came in March 2008, so what are the causes of this collapse?

The company started to have problems when the company drove into hedge fund business, the type of investment that invests in risky assets and uses a leverage to increase return. The company borrowed money and invested a lot of money in a collateralized debt obligation (CDO), derivatives that the value based on mortgage-backed securities because they believe that they can generate a huge return on this investment. However, things went wrong. In April 2007, the company held $20 billion of CDO in their portfolio, but the assets’ value started to drop since 2006 because the housing bubble started to burst and the housing prices plummeted. Moreover, in November 2007, Bear Stearns’ reputation was ruined by an article from Wall Street Journal that criticized Bear’s CEO, James Cayne. It claimed that James Cayne was addicted to marijuana and did not care about saving the company.

On December 20, 2007, Bear Stearns announced a huge loss of $854 million for the fourth quarter and $1.9 billion write-downs (devaluating of the asset) of its subprime mortgage holdings. After struggling for a while, the company has problems on liquidation. In other words, the company did not have enough cash to run a business. The collapse of the company could impact other over-leveraged investment banks which will affect the entire economy. As a result, with the help of Federal Reserve, Bear Stearns was sold to JP Morgan Chase in March 2008, and that was the end of one of the famous investment banks. (4)

Why did the Fed bailout AIG and how was it carried out?

Before 2008, who is going to believe that one of the biggest multinational insurance corporations with operations in more than 80 countries known as the American International Group, (AIG), will go on the verge of bankruptcy. On February 28, 2008, AIG announced 6.2 $ billions in earning, approximately 2.39$ per share, and stock close at 50.15 $ that day. However, less than seven months later, the company almost went bankrupt, and the stock was traded at less than a dollar per share (2), so what happens??

AIG was one of the biggest issuers of Credit Default Swap (CDS) on subprime loans at that time. The company looks CDS as “gold” and free money because their financial model believes that the underlying security, housing loan, would never go default. However, they were wrong. When the housing bubble started to burst, many mortgages defaulted and created a huge create a huge loss to the company because the company’s portfolio had about $526 billion of CDSs. Even though AIG had more than enough assets to cover the swaps, it could not sell them before the swaps came due, so the AIG needed to raise more capital in order to pay for the debt. Unfortunately, the investor was scared of the situation; they sold their shares which made the company even more difficult to raise money to cover the swaps. However, AIG survived from this situation thanks to the help of the Federal Reserve that provided a huge amount of money to the company, but why it did that ??

(Source: "U.S. to Take Over AIG," The Wall Street Journal, September 17, 2008.)

Ben Bernanke, Former Federal Reserve Chairman, was outraged about the bailout of AIG than anything else in the recession. He stated that AIG took risks with unregulated products while using cash from people's insurance policy. Even though the US government do not want to rescue the company, there is no

What is the moral hazard risk people talked about after the Fed's rescue of several financial institutions?

The 2008 financial crisis caused by several factors in financial sectors in the US. Many parties involved with the collapse of the financial system. However, one of the greatest causes of this disastrous event was Moral Hazard.

“A moral hazard exists when a person or entity engages in risk-taking behavior based on a set of expected outcomes where another person or entity bears the costs in the event of an unfavorable outcome.” (Source: The Fall of the Market in the Fall of 2008)

Before the financial crisis, financial institutions expect the official authorities to support them in bad situations in order to avoid the collapse which will highly affect the rest of the economy. As a result, many large investment banks and financial institutions invested in risky loans, traded in risky derivatives, and operated inefficiently because they knew that if they fail, someone will rescue them.

Some banks and financial institutions consider themselves as “Too big to fail.” They believe that they are so essential to the economy, so the government would not let them go bankrupt. As a result, the financial sectors would likely to invest in riskier assets to gain their return as much as they could, and if something went wrong, they know that the government will rescue them from the collapse to reduce negative impacts that will spread to the entire economy.

The other form of moral hazard is that banks accepted risky assets as collateral and underwrote the mortgages with weak standards. In general, banks should lend money to the borrowers under carefully analyze. However, banks lower their standards and made riskier decisions because they believe that they can pass on the risk to the buyers, which in this case is investment banks. In the other word, banks underwrite loans with the expectation that another party or buyer would likely bear the risk of default. This kind of practices creates a moral hazard and lead to the subprime mortgage crisis at the end. (6)

References

(2) The AIG Bailout by William K. Sjostrom :: SSRN. (n.d.). Retrieved from https://ssrn.com/abstract=1346552

(4) Amadeo, K. (2008, September 19). How a Bank That Survived the Depression Started the Great Recession. Retrieved from https://www.thebalance.com/bearn-stearns-collapse-and-bailout-3305613

(5) Amadeo, K. (2009, March 19). This Bailout Made Bernanke Angrier than Anything Else in the Recession. Retrieved from https://www.thebalance.com/aig-bailout-cost-timeline-bonuses-causes-effects-3305693

(1) Amadeo, K. (2011, August 27). What Caused the 2008 Financial Crisis and Could It Happen Again?. Retrieved from https://www.thebalance.com/2008-financial-crisis-3305679

(3) The Causes and Effects of the 2008 Financial Crisis [Video file]. (2012, July 23). Retrieved from https://www.youtube.com/watch?v=N9YLta5Tr2A

(6) Investopedia. (2017, October 20). How did moral hazard contribute to the 2008 financial crisis?. Retrieved from https://www.investopedia.com/ask/answers/050515/how-did-moral-hazard-contribute-financial-crisis-2008.asp

(8) Retrieved from https://www.usatoday.com/story/money/business/2013/09/08/chronology-2008-financial-crisis-lehman/2779515/